By the SandRose Editorial Team

Ever since the commercialization of oil and gas through the drilling of the Drake well in Pennsylvania in 1859, hydrocarbons have become a cornerstone of the global economy. While most may only consider their applications as fuels and sources of power, our modern lifestyle is one that is fundamentally reliant on hydrocarbon products for the production of materials such as plastics, steel, and cement, not to mention their instrumental role in enabling other crucial endeavors such as agriculture and food production, pharmaceuticals, and all manner of consumer products.

As hydrocarbons have become deeply ingrained within the quality of life we have become accustomed to, however, the industry has also been heavily scrutinized as climate change has been catapulted into the forefront of global debates on policy and governance. While there is no denying the importance of tackling climate change head on, a sober perspective is required to appreciate the role that hydrocarbons play in a sustainable future for all. As an industry that is notorious for its cyclic downturns, and in the face of this mounting questioning, how will it showcase its resilience and relevance on the global stage in the decades to come?

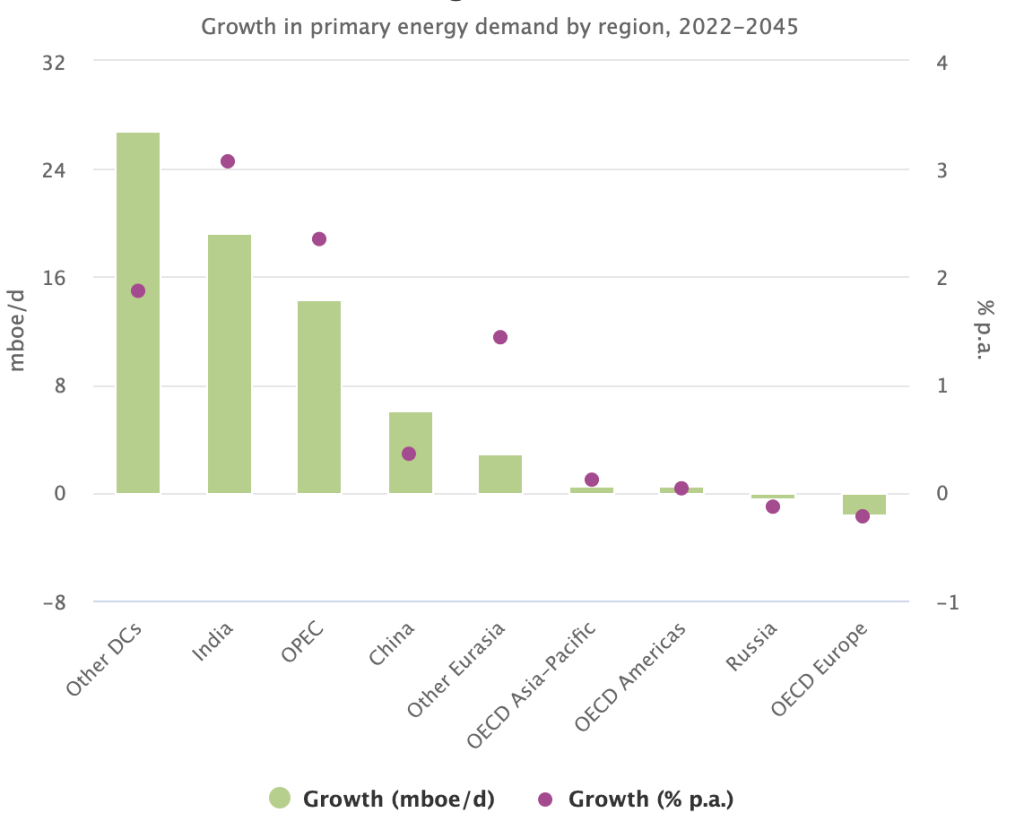

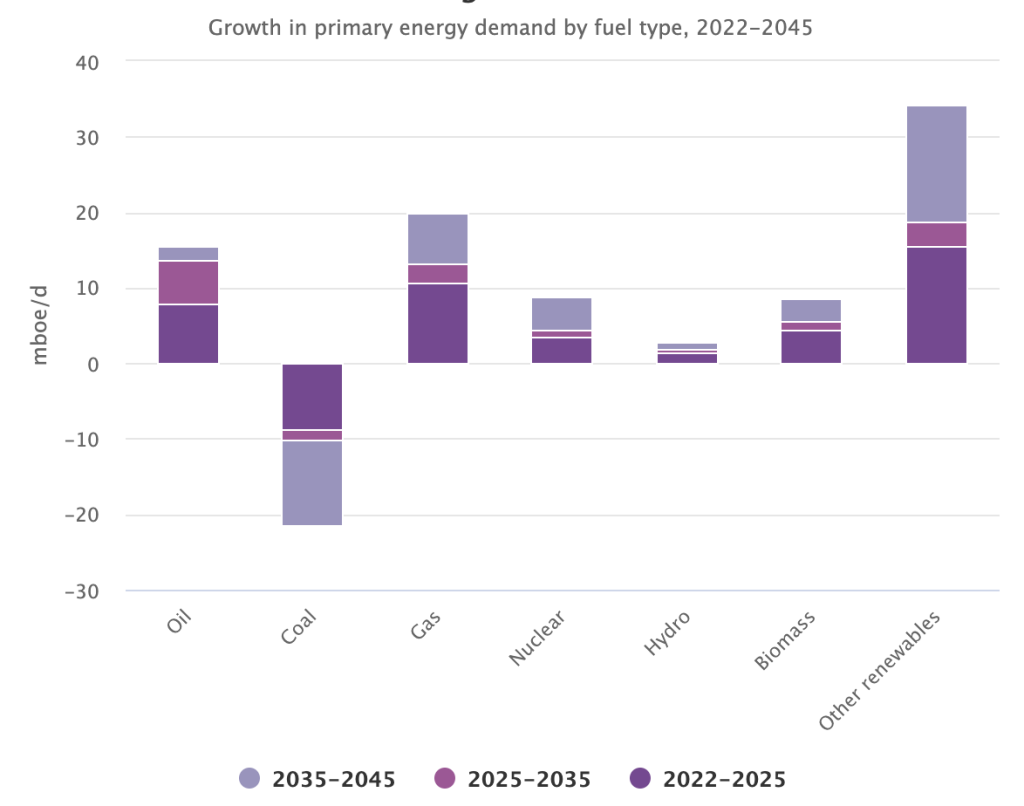

The foundation of this debate is predicated on a few key pillars, the first of which is the basic economics of supply and demand. On the demand side, the current global market for hydrocarbons is estimated at slightly over 100 million barrels per day (bpd). While there is some contention in regards to which direction this figure is likely to move in the future, there are a few realities that can begin to elucidate the answer. The main drivers of any decrease in demand are mainly a function of (a) policy changes favoring alternative sources of power, fuel, and materials, (b) efficiency improvements in technologies relying on hydrocarbons (such as the internal combustion engine), and (c) disruptive technologies that may create a substantial difference in the levelized cost of energy from non-hydrocarbon sources.

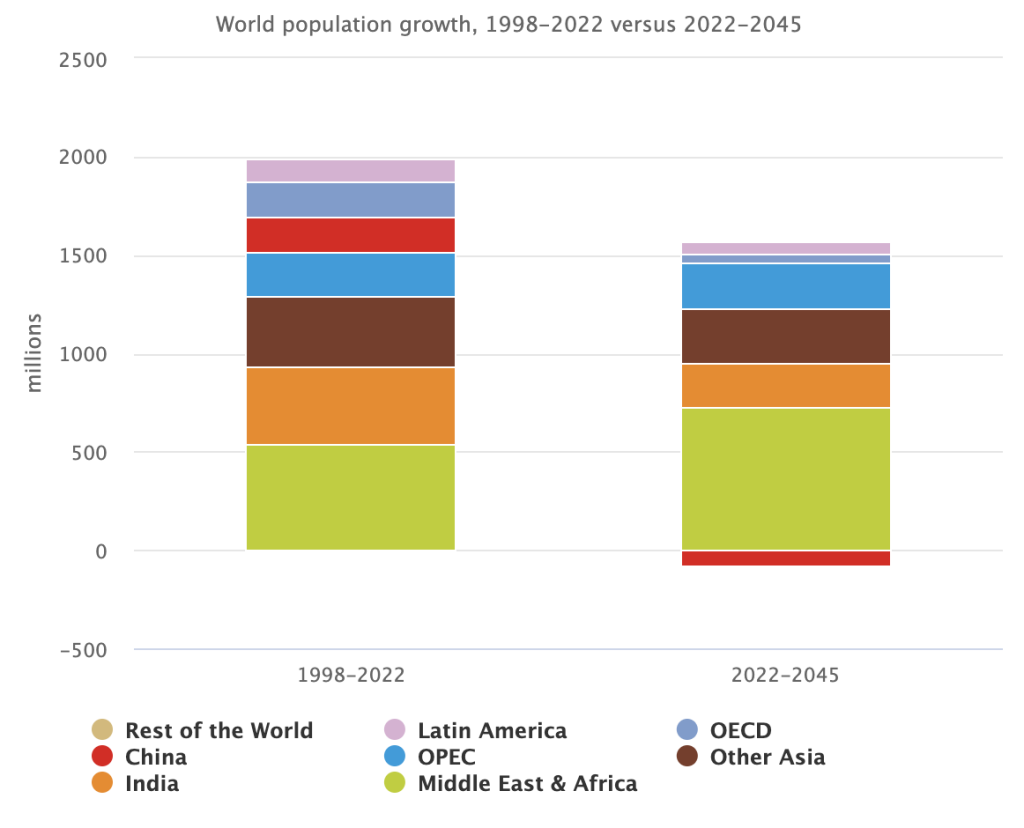

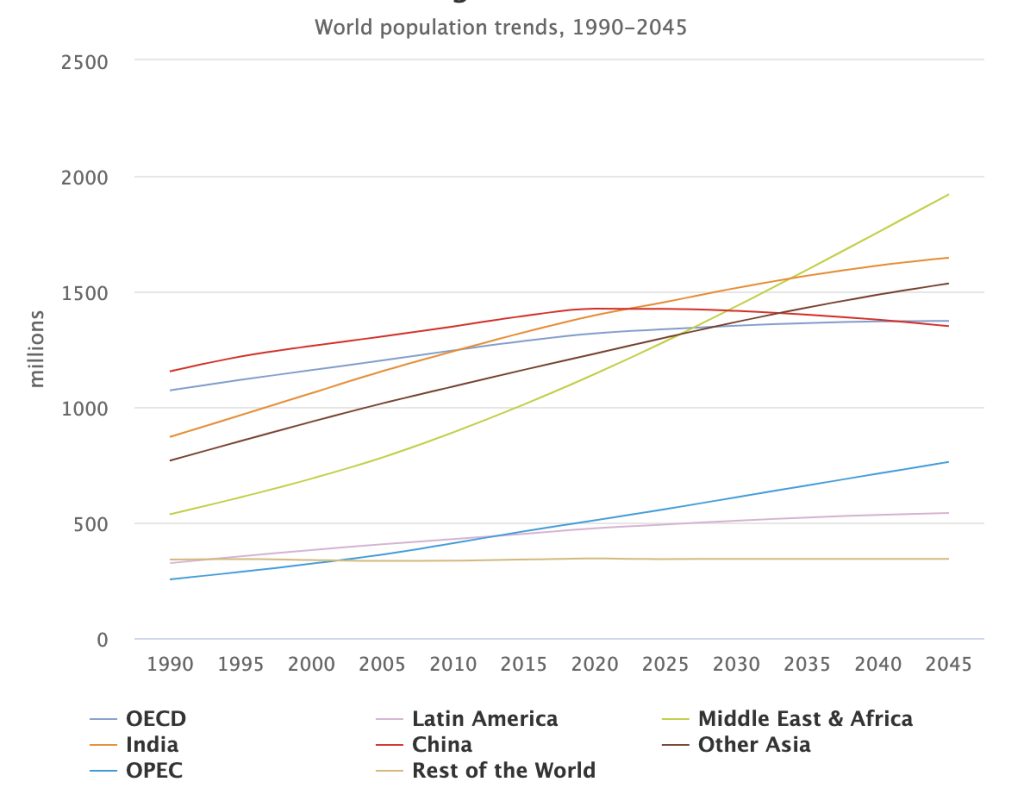

Historically speaking, the net result of these factors has not yielded any substantial or long-lasting diminishment in global demand. On the other hand, there are several compelling drivers of increased hydrocarbon demand. The global population is poised to increase by approximately 2 billion people by 2050. The bulk of that increase will come from an expanding middle class primarily from Asian and African markets in countries with rapidly growing and industrializing economies, often referred to as the global south. This expanding middle class is expected to generate a higher demand (on both a net and per capita basis) on consumer products, fuels, and power compared to the current figures.

“This expanding middle class is expected to generate a higher demand (on both a net and per capita basis) on consumer products, fuels, and power compared to the current figures.“

Examining the supply end of the equation, there have been a steady slew of new hydrocarbon discoveries across different geographies, especially in the Middle East with many of the world’s highest volume producers. Not only does almost half of the world’s supply come from this region, but the average production costs also tend to be lower compared to the global average. This trend is unlikely to change in the near future as technology supports ongoing exploration efforts, and by raising the proportion of economically recoverable resources from existing fields.

In most western (or global north) economies, as exemplified by the OECD block, there is a contrast in terms of policies that encourage or subsidize renewable energies over hydrocarbons. Despite forecasts of increasing energy demand, most western nations have observed declining investments in the upstream sector. Conferences such as the annual COP have become a hotly contested battle ground for the debate on what path should be taken towards a sustainable future. What has become clear is that there is no one-size-fits all approach for all countries looking to manage their emissions while still providing for their citizens in a manner that is sustainable, affordable, and accessible (hence the energy trilemma).

“There is no one-size-fits all approach for all countries looking to manage their emissions.“

This also begs the question of how to equitably finance the energy transition for all countries. This is a particularly controversial point, considering the global north has historically benefited the most from hydrocarbons, and therefore arguably bears the burden of a higher proportion of cumulative emissions. While some analysts and policy makers see a rapid transition to renewables as the answer, other voices in the conversation see hydrocarbons as a long-term primary component of the transition. They see the transition as more of an energy expansion, welcoming other sources of energy including renewables, while offsetting or otherwise managing the emissions associated with hydrocarbon production and utilization.

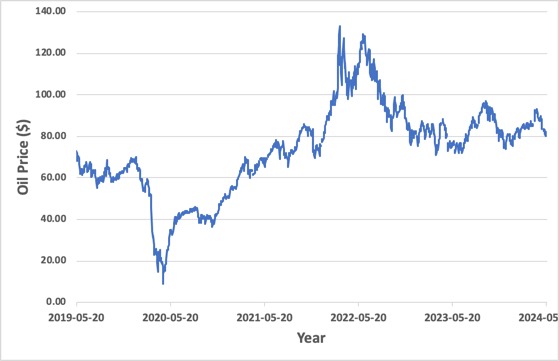

As mentioned previously, the oil and gas industry is no stranger to downturns and has experienced many different varieties of setbacks: from near-zero prices during the pandemic, intentional attacks on facilities such as pipelines and refineries, to wide-sweeping financial crashes such as in 2008. Each of these setbacks has taught those in the industry painful and valuable lessons. The common element across each of these varied challenges is that the industry has bounced back from each and every one of them.

“The oil and gas industry is no stranger to downturns.“

While individual setbacks, especially black swan events such as the pandemic, are difficult if not impossible to predict, what is certain is that there will be more difficulties to come. While the industry may be susceptible to financial crashes and the volatility of the market, it has invariably pulled through these challenges because the alternative is a non-starter: if the world could move forward without hydrocarbons, it would have done so by now.

“If the world could move forward without hydrocarbons, it would have done so by now.“

Beyond the irrevocable necessity of hydrocarbons for powering our world and providing us with the quality of life that has become normalized in the 21st century, the oil and gas industry’s resilience has also been supported by its own intentional evolution. From an operational perspective, the industry utilizes some of the world’s most complex and interconnected supply chains. This was heavily disrupted by the pandemic, and yet several key players such as Aramco adapted largely thanks to localization programs such as iktva. Elsewhere, some supermajors have opted to expand their portfolio to extensively feature renewables. Most supermajors have also pursued more robust integration across their value chain, starting with upstream, to refining, all the way to retail refueling stations that often feature electric vehicle (EV) charging infrastructure. Industry stalwarts such as Aramco have also made immense investments towards diversification through their venture capital fund, Aramco Ventures, which features several ventures well beyond the scope of the industry itself.

The oil and gas industry has a hefty task on its shoulders. It is expected to provide fuel, power, and materials to meet the growing needs of a global population that is simultaneously erupting in size all while placing heavier expectations on the industry’s expedited action in response to climate change. Those with a broader perspective of not only the industry, but also the makings of the 21st century quality of life will have realized that (a) the world is not yet prepared to step away from hydrocarbons, and (b) the world does not have a hydrocarbons problem, but rather an emissions problem.

“The world does not have a hydrocarbons problem, but rather an emissions problem.“

A more sustainable solution to the current energy trilemma and transition should therefore involve sufficient upstream investment on a global scale. For this to be successful, there should also be continued expansion in renewables, and in emissions management technologies such as direct air capture (DAC). The key to a successful transition lies in a multi-modal, multi-speed approach that allows for the necessary flexibility for each country to tailor its own solutions for itself. This can only happen in the context of global cooperation across investment, technology, and policy domains in a manner that recognizes the world’s shared interests and prioritizes them over short-term gains.

“The key to a successful transition lies in a multi-modal, multi-speed approach that allows for the necessary flexibility for each country to tailor its own solutions for itself.“